Shortcomings of Fiscal Activism Exposed in Important New Book

posted by Tim Congdon on April 27, 2019 - 1:51pm

Low growth rates of banking systems and the quantity of money, broadly-defined, continue to characterize the world’s major economies. 2019 will see growth in world output, but it may be 3% or less, down from the 3.8% recorded in 2017 and 3.6% in 2018. (These figures are from the International Monetary Fund’s World Economic Outlook database.) The Eurozone remains the most problematic region in the world economy, with most forecasts converging on a 1% figure for 2019 growth, while Italy remains the most problematic large nation in the Eurozone, with a consensus that 2019 will see hardly any growth at all.

Much commentary points out the difficulty of pursuing expansionary monetary policy in the Eurozone, given that the European Central Bank’s main refinancing rate is zero. Since interest rates cannot be pushed any lower, the answer is said to be the activation of fiscal policy. Indeed, this Keynesian argument – on the need to deploy fiscal policy because of the supposed “impotence” of monetary policy at low or zero interest rates – has also been heard in the contexts of Japan, the United States of America and the United Kingdom at various times in the last 30 years. Advocates of fiscal policy activism should read a recently published book on Austerity: when it works and when it doesn’t by three Italian authors, Alberto Alesina, Carlo Favero and Francesco Giavazzi. The Alesina, Favero and Giavazzi volume is almost certainly the most important contribution to the international policy debate to appear in 2019 and perhaps in the current decade; it represents a huge challenge to mainstream Keynesian thinking. (The book follows up previous work in the same vein. See, for example, the paper on ‘Can severe fiscal contraction be expansionary?: tales of two small European countries’, by Giavazzi and Marco Pagano, in Blanchard and Fischer [eds.] NBER Macroeconomics Annual, 1990. It was this 1990 paper which led to the phrase, “expansionary fiscal contraction”.)

When Keynesians propose the activation of fiscal policy, they mean that government spending and budget deficits should be increased to counter busts, and that government spending and budget deficits should be reduced to neutralize booms. In their view cuts in government spending to limit budget deficits should never be undertaken in recessions. To be blunt, they regard so-called “fiscal contraction” in a recession as economic illiteracy. The key finding of Alesina, Favero and Giavazzi inAusterity is that cuts in government spending that reduce the budget deficit by 1% of GDP have only a modest negative impact (of ½% of GDP or so) on national output in the next year or two, and hardly any negative effect at all three or four years later. This finding is obtained from a large-scale empirical exercise, involving a sample of “200 multiyear austerity plans carried out in 16 OECD countries from the late 1970s to 2014”. Keynesians cannot easily dismiss what Alesina, Favero and Giavazzi are saying, since the body of evidence is immense, and the sample cannot be biased when it extends over so many countries and such a long period. But – if these three Italians (and other like-minded colleagues at the Bocconi University, Milan) are right – the copybook maxims of Keynesian fiscal policy are junk. The Bocconi position is a radical challenge to textbook Keynesianism.

On 10th April I attended an event organized by the Centre for Economic Policy Research and Imperial College Business School at which Professor Giavazzi launched the new book. He was interviewed by Sir Charles Bean, former deputy governor of the Bank of England and a member of the Office of Budget Responsibility. For Bean, and in fact many others who have followed the UK policy debate in recent decades, the Bocconi results may not have been a total surprise. The debate about the UK’s 1981 Budget – which engineered a sharp reduction in the budget deficit despite a recession and was met by a letter of protest (to The Times newspaper) from 364 economists – presaged that which is now taking place between the Italians from Bocconi and such East Coast Keynesians as Paul Krugman, Jo Stiglitz and Larry Summers.

Perhaps the most influential defenders of mainstream Keynesianism in the UK have been Professor Lord Skidelsky of Warwick University, Keynes’ biographer, and Martin Wolf of the Financial Times. Readers of my own work will know that I crossed swords with Wolf’s 2013 Wincott Memorial Lecture in a 2015 paper published in The Journal of Economic Affairs. The 2015 paper recalled the Giavazzi phrase, since it was entitled ‘In praise of expansionary fiscal contraction’. In his recent book on Money and Government Skidelsky focusses on me rather than the Bocconi economists as a critic of fiscalist Keynesian. Correctly, he quotes me as saying, “Forget about fiscal policy. It [i.e., meaning so-called ‘expansionary fiscal action with a widening of the budget deficit] doesn’t do any good to short-run economic activity…and may do a lot of long-run harm.” That is exactly what I believe, and have indeed believed for over 40 years.

Obviously, this continuing and growing debate – about the relative effectiveness and usefulness of monetary and fiscal policies – is of massive importance to the conduct of macroeconomic policy in coming years. The Institute of International Monetary Research has invited Lord Skidelsky to give a public lecture on economic policy-making on the evening of 12thNovember in London. We are hugely grateful to Lord Skidelsky that he has accepted the invitation. On 13th November a one-day conference on ‘Fiscal policy vs. monetary policy: which is best?’ will be held, also in London, under the Institute’s auspices. We hope that Lord Skidelsky’s public lecture and the conference will enable all sides to be heard, and that the result will be some clarification of the issues. We will be sending out formal invitations nearer the time.

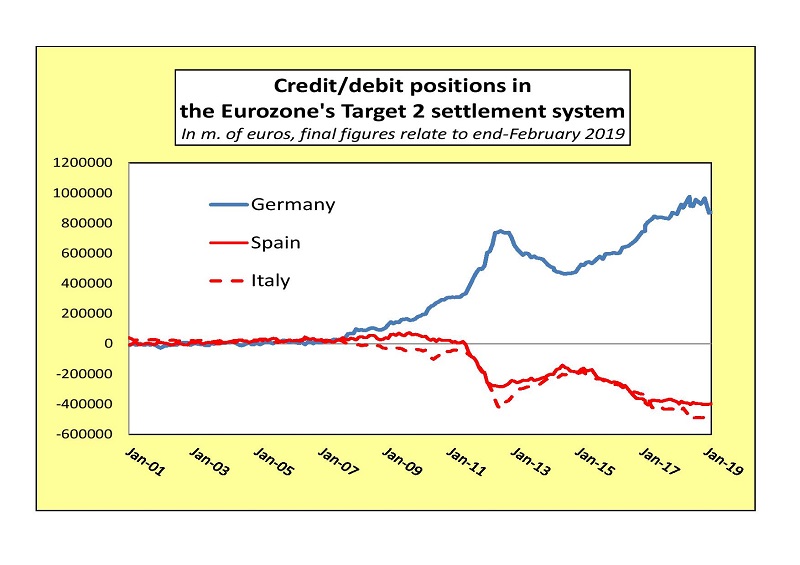

The standard note on global monetary trends shows that money growth in the USA and the Eurozone has been more resilient than expected so far in 2019, but money growth in the less significant countries of Japan and the UK has been very weak. Below is the usual monthly chart on the Eurozone’s Target 2 settlement system.

The figures for end-February are much the same as those for end-January. On this benchmark of market confidence, little change has occurred in recent months in the relative positions of Germany, Italy and Spain. (If you are surprised and puzzled about markets’ apparent equanimity, so am I.)