The Powell Cave-in

posted by Karim Pakravan on July 13, 2019 - 4:38pm

The most recent semi-annual testimony to Congress by Jay Powell, the chairman of the Fed, was essentially a cave-in to pressure from both President Trump and Wall. Street The president is looking to save what he considers his shining economy and stock market going into the 2020 election, while Wall Street wants to extend the bull market at a time of flagging profits growth and uncertain economic prospects. While Wall Street economic analysts and even the New York Times have cheered the prospect of a “ Powell Put” in the form of one or more cuts in the benchmark (Fed funds) rate, a few (including Mohamed el-Erian in a recent piece) have questioned the need or the wisdom of such a shift in monetary policy.

Essentially, the argument of Powell and the Fed “doves” goes like this: faced with a potentially faltering U.S. economic expansion and rising global risks, the Fed should be pro-active by providing insurance by cutting its benchmark Fed funds rate. Such a move would boost investment, fuel up the mortgage market and provide a measure of insurance against an economic downturn. However, these arguments do not hold water.

- Usually, the Fed intervenes in the economy when there is evidence of a significant slowdown or recession. This happened in 2000 and 2008. In each of these cases, the Fed cut rates sharply to counter the economic downturn. This is the first time the Fed loosens up monetary policy in the face of decent data and while the economy is still enjoying solid growth and record low unemployment.

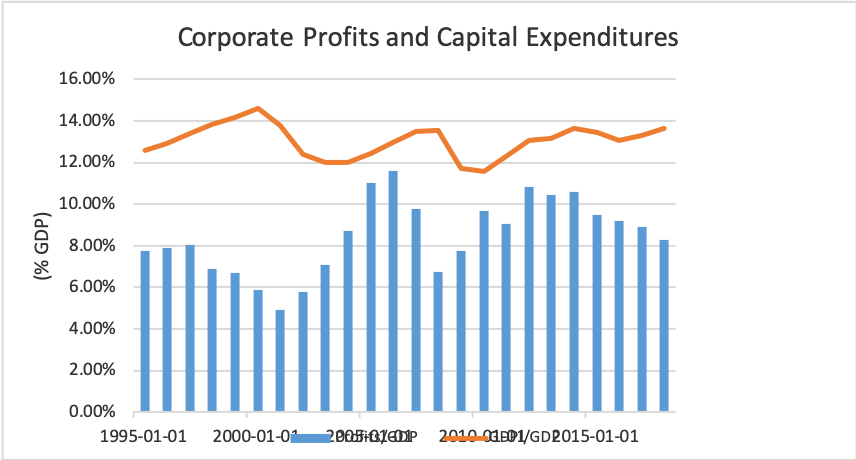

- Recent history shows us that while record low interest rates and quantitative easing helped the economy recover from the deep 2008-2009 recession, they have done little to boost investment. In the later stages of the recovery. In fact, the share of domestic investment in GDP has remained relatively flat, at around 13% over the past few years, despite record profits.

- In the same vein, the massive 2017 corporate tax cut has not resulted in a boost in investment. In fact, the combination of extra-easy liquidity and record profits has resulted in an unprecedented wave of shares buyback in 2018 and the first few months of 2019. This led to an increased gap between equity markets trends and economic and business fundamentals.

- A rate cut will mostly be dissipated on further share buybacks, with little impact on the real economy. In fact, the main impact will most likely be the worsening of income and wealth inequality.

While the prospect of a rate cut has already propelled the stock market to new record highs, we should not confuse the health of the stock market and the strength of the economy. Former Fed chair Bernanke warned in 2004 against following markets blindly in order to learn about the economy.

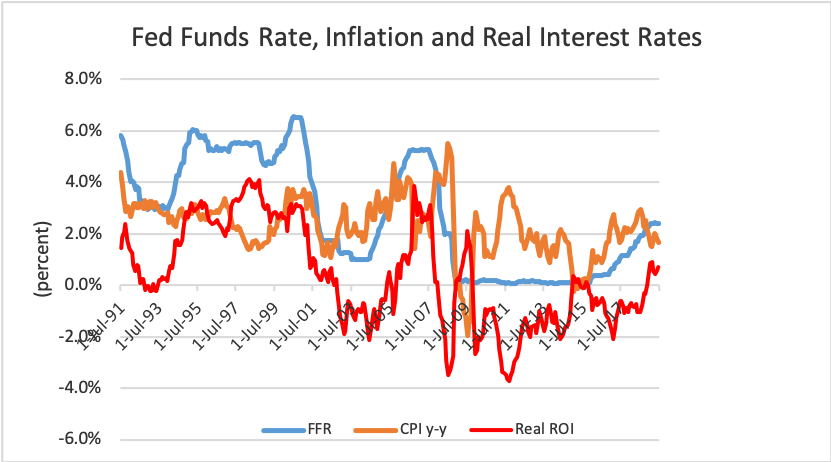

Market analysts are projecting three rate cuts totaling 75 basis points by year end. This will leave the benchmark rate at 1.50%, leaving the Fed very little room to maneuver if we face a more serious downturn. (In both 2000 and 2008, the benchmark rate was over 5% at its peak).

In conclusion, a Fed rate cut at this point of the economic cycle is not necessary. In fact, it could be counterproductive, since most of the benefits would go to Wall Street, without a real impact on the economy. Moreover, by feeding the asset bubble, it would contribute to a worsening of the economic imbalances. So, while it is understandable that Wall Street and the Trump administration are cheering newly acquired dovishness of the Fed chair and its Board, Powell would be doing a disservice to the nation by promising rate cuts.