The IMF World Economic Outlook: Is Pessimism Warranted?

posted by Karim Pakravan on April 18, 2019 - 3:59pm

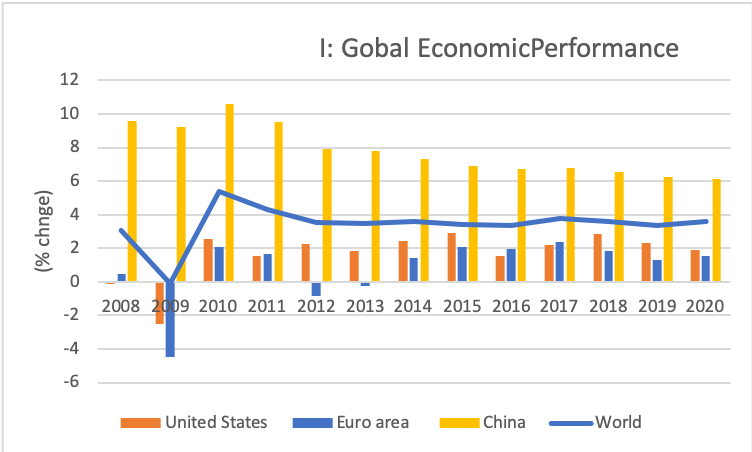

The U.S. post-crisis expansion is now entering its tenth year, and the global economy experienced a two-year synchronized upswing in 2017 and the first half of 2018. The global economy is still growing, but there are signs that both cyclical upswings are running out of steam. However, there are divergent view among analysts and policymakers about the short and medium-term prospects for the global economy, as well as about the needed policy responses. The most recent International Monetary Fund (IMF)/World Bank meeting was an opportunity for the IMF to offer its views of the global economic and financial landscape through its twin publications, the World Economic Outlook (WEO) and the Global Financial Stability Report (GSFR). The April WEO underscored a moderation of global growth in the next two years. According to the IMF, global output growth softened in the second half of 2018 from 4% in 2017 and 3.8% in the first half of 2018 to 3.6% in the second half of the year. Furthermore, the IMF revised downward its growth projections for 2019 and 2020—by 0.4%, to 3.3% in 20129 and by 0.1% to 3.6% in 2020—also note that the IMF never projects a recession.

The IMF underscored the faster-than-expected waning of the 2017-18 cyclical upswing, citing monetary tightening by the major central banks, Brexit, the slowing of the growth in global trade, rising trade tensions between the United States and its major trading partner, the decline in global business confidence and rising policy uncertainties.

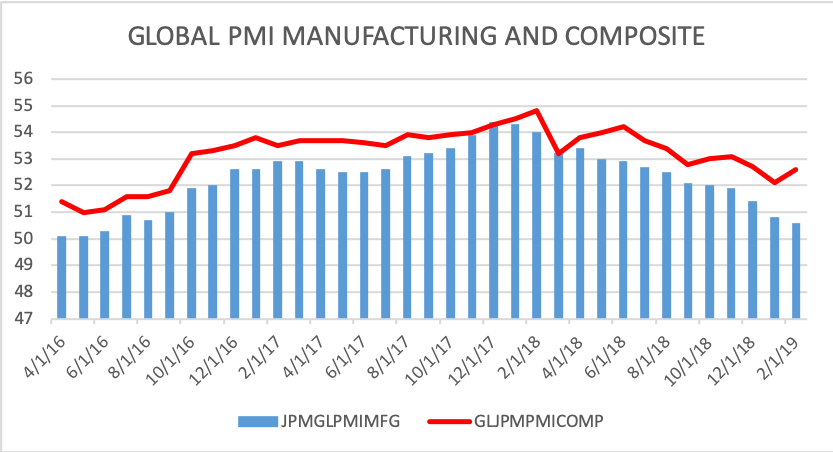

However, the recent data is mixed and analyst views on the short and medium-term prospects of the global economy are diverging. On one hand, we are seeing softer economic growth in China and the Eurozone and the weakness in global manufacturing. (The JPMorgan Global Manufacturing PMI fell from a high of 54.8 in February 2018 to 52.1 at the end of January 2019.) The impact of the 2017-18 fiscal stimulus in the United States is fading and recent U.S. economic indicators are mixed at best. Furthermore, the Eurozone economy is slowing down. The German economy, (which accounts for a third of the Eurozone’s economic output) experienced a contraction in the fourth quarter of 2018 and was flat in the first quarter of 2019. Most recently, the German Ministry of Economy cut its 2019 growth forecast by half, to 0.5%. In addition, the latest PMI readings for the United States and the Eurozone underscore continued weakness in these economies. On the other, recent data on the Chinese economy show that the stimulus measures introduced in the past few months have resulted in a short-term economic boost, with GDP growing by 6.4% (year/y) in the first quarter of the year. The possibility of a trade deal between the United States and China has increased and overall financial conditions remain accommodative.

In particular, financial risks seem to be underestimated. First of all, while the major central banks have softened their stance and moved back to monetary accommodation, they have little room for maneuver. For example, in the previous recession in 2008, the Fed was able to cut the Fed Funds rate from 5.25% to zero in a matter of months. Today, the Fed Funds rate is 2.50-2.75%, yet the Fed is under strong political pressure to cut rates. Second, according to the GSFR, we have seen a surge in lower-rated and covenant-lite debt issuance in the United States. So, while corporate balance sheets are stronger, they remain vulnerable to a serious economic downturn. The GSFR also cited concerns about sovereign debt in the Eurozone, in particular in the case of Italy.

These uncertainties have led to diverging signals from equity and bond markets. The major equity markets have recovered from the end-2018 bloodbath, but are struggling to regain their past peaks. At the same time, the U.S. bond markets are flashing red signals, with a flattening (and even temporary inverting) of the yield curve, indicating a higher likelihood of a recession in the next 6-18 months.

Overall, it seems that the global economy is on a knife-edge. On balance, Nevertheless, risks remain, and the IMF sees these risks skewed to the downside. Furthermore, the IMF’s softer economic forecast is indicating a potential shift to a global slowdown, with heightened probability of a recession in both the United States and the eurozone, with continued underperformance in the Japanese and UK economies.