The IMF and the Minsky Moment

posted by Karim Pakravan on October 20, 2017 - 4:43pm

The IMF published the latest versions of its flagship publication on the occasion of the IMF/World Bank Annual Meeting that just concluded in Washington. —the World Economic Outlook, WEO, and the Global Financial Stability Report, GFSR. While the WEO focuses on global macroeconomic trends, the GSFR is an in-depth analysis of the health of the global financial system. The WEO’s tone is upbeat, underscoring the strengthening of the global synchronized cyclical upturn. The WEO projects that global output will grow by respectively 3.6% and 3.7% in 2017 and 2018.

The GFSR is less sanguine, confident about short-term financial stability, but concerned about medium-term market vulnerabilities. The IMF considers that the global financial system has considerably strengthened as a result of the cyclical upturn in growth, regulatory enhancements and extraordinary policy (monetary) support. As an example, the so-called G-SIBs (Globally Systemically Important Banks) have added $1 trillion in capital since the financial crisis. At the same time, the hunt for yields, rising asset valuation and growing leverage are a cause for concern. In other words, the question is whether we are in a “Minsky Moment”[1]?

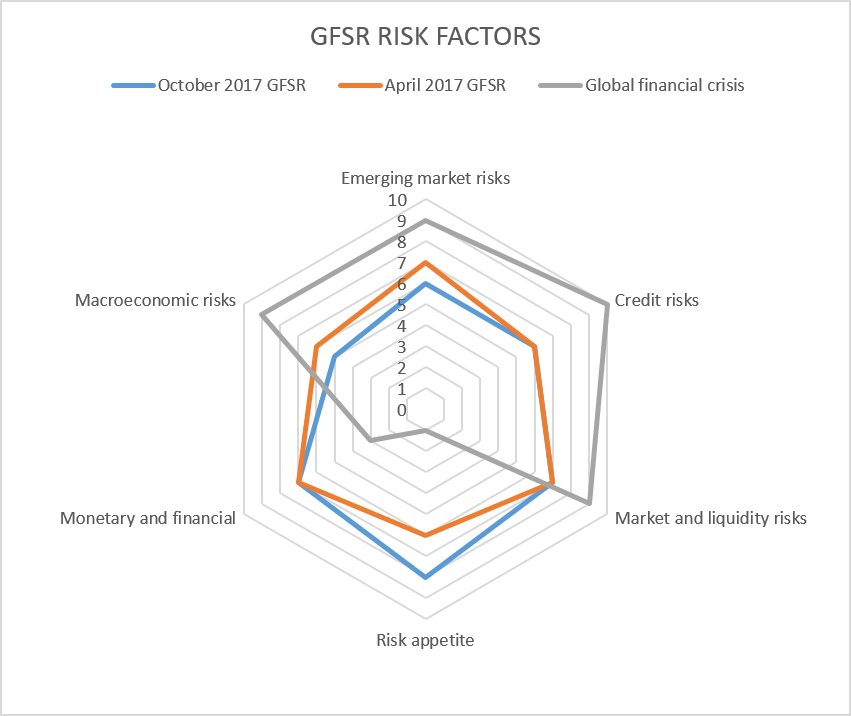

Fig.1: GFSR Risk Web

According the GFSR’s analysis, large-scale monetary accommodation has led to a leverage-fueled surge in asset prices and an unprecedented decline in market volatility. Among the G-20, total non-financial debt has increased by $60 trillion since 2006, to 235% of GDP—and 260% of GDP for the advanced countries. Corporate and sovereign debt accounted for almost $50 trillion of the debt increase. While high debt levels are not problematic per se, debt servicing is a cause for concern.

Monetary authorities in developed countries, especially the Big Four (Federal Reserve Bank, European Central bank, Bank of England and Bank of Japan) have been at the center of the extraordinary monetary policy support, essentially quadrupling their collective balance sheet—increasing in the process their holdings of government debt from 10% to 37% of GDP since the financial crisis. The process of monetary normalization, which has barely started, is expected to be very gradual. This speed of central bank’s balance sheet adjustment involves a trade-off. On one hand, an abrupt change could cause turbulence in financial markets. On the other, a too-slow pace of change will result in continued buildup of financial excesses.

The GFSR considers a crisis scenario which has all the marks of a “reverse Minsky”: a vicious circle of credit crunch, deleveraging, sale of assets and asset prices collapse. The IMFs “Global MacroFinancial Model” forecasts that such a crisis would have a macroeconomic impact of about one-third of that of the 2008 financial crisis. However, even without knowing the model assumptions, one can argue that this is an underestimation of the potential impact.

The GSFR recommends a series of measures to reduce the likelihood of the crisis:

- Major centrals should ensure a gradual, smooth and well-telegraphed monetary policy normalization process

- Financial Regulators should deploy macroprudential measures to strengthen the resiliency of banking systems and tighten the regulation of non-banks

Of course, the necessary condition for continued financial stability is dynamic growth. To this end, the final communique of the IMF meeting states: “The welcome upturn in global activity provides a window of opportunity to tackle key policy challenges and stave off downside risks, including by ensuring appropriate buffers, and to maximize returns on structural reforms to raise potential output. We reinforce our commitment to achieve strong, sustainable, balanced, inclusive, and job-rich growth. To this end, we will use all policy tools—monetary and fiscal policies and structural reforms—both individually and collectively.”

The IMF and the collective group of economic and financial policymakers may be patting themselves on the back for the state of the world economy and financial markets, but these reports raise important issues that need to be addressed if we want to avoid a repeat of 2008.

[1] Minsky was a long-ignored economist who postulated in 1974 that financial markets are inherently unstable, going through five phases: displacement, boom, euphoria, profit-taking and crisis. In other words, credit-fueled asset bubbles collapse following the exhaustion of a credit expansion. The first four phases are what has been called a “forward Minsky Journey”, and the last one (and its aftermath) a “reverse Minsky Journey”.