China's Currency Manipulation? Trump is Two Years Late

posted by Karim Pakravan on February 13, 2017 - 10:35am

One of the oft-repeated themes of Candidate (then President) Trump is that the world has been taking advantage of us at every turn, and that China is the main culprit. The evidence presented is that China has been systematically manipulating its currency to boost its exports and discourage imports, thus contributing to the massive U.S trade deficit. However, the evidence is a dollar short and a couple of years late. If anything, China has been struggling in the past 18 months to prevent its currency from depreciating too rapidly.

Two forces have been at play. First, the financial shock in June 2015, and second, China’s drive to internationalize the RMB.

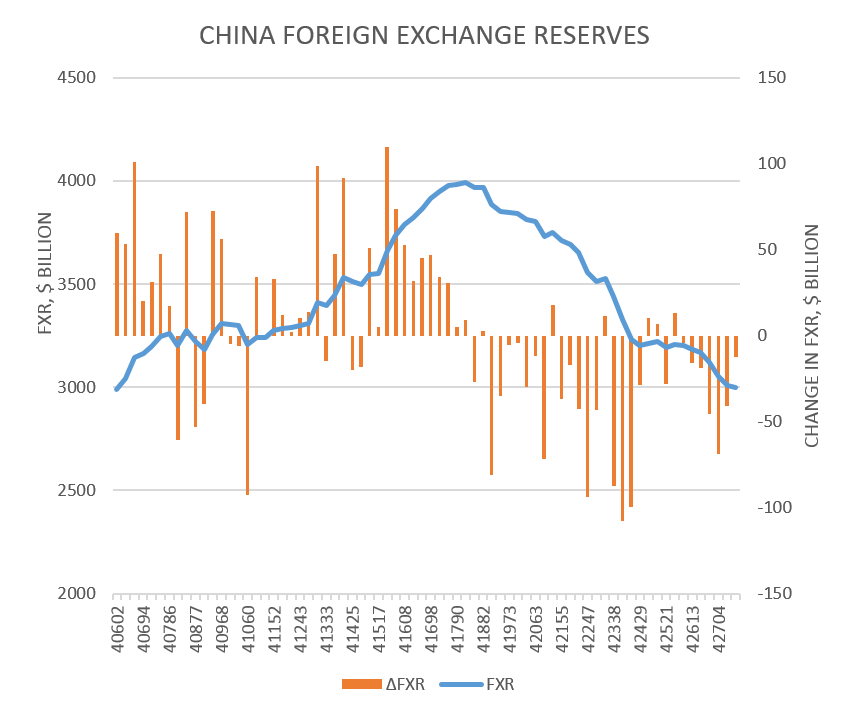

The June 2015 Financial shock: A sharp slowdown in growth in 2015 precipitated a sharp stock market and yuan pullback in June 2015. The Shanghai composite index crashed by 47% between its all-time peak on June 12, 2015 to its low point on February 5, 2016. The yuan lost 5.6% relative to the dollar over the same period. The stock market crisis abated in 2016, with the markets stabilizing at lower levels. However, despite heavy intervention by the People’s Bank of China (PBoC, the Chinese Central bank) , which cost the PBoC approximately $500 billion in foreign exchange reserves over the July 2015 to March 2016, the yuan continued to depreciate, both against the US dollar and on a trade-weighted base. Overall, the Chinese currency has lost 12% against the US dollar in the past three years—and 8 on a trade-weighted basis since mid-2015.

CNY Internationalization: Over the past few years, the Chinese authorities liberalized the capital account in order to promote the yuan as an international currency. This effort culminated in the inclusion of the yuan in the SDR basket of currencies in October 2016, at which point the Chinese yuan had become the fifth most traded currency, with a 2% global market share—behind the yen, but ahead of the Canadian and Australian dollars. At the same time, the Chinese companies went on an overseas investment spree.

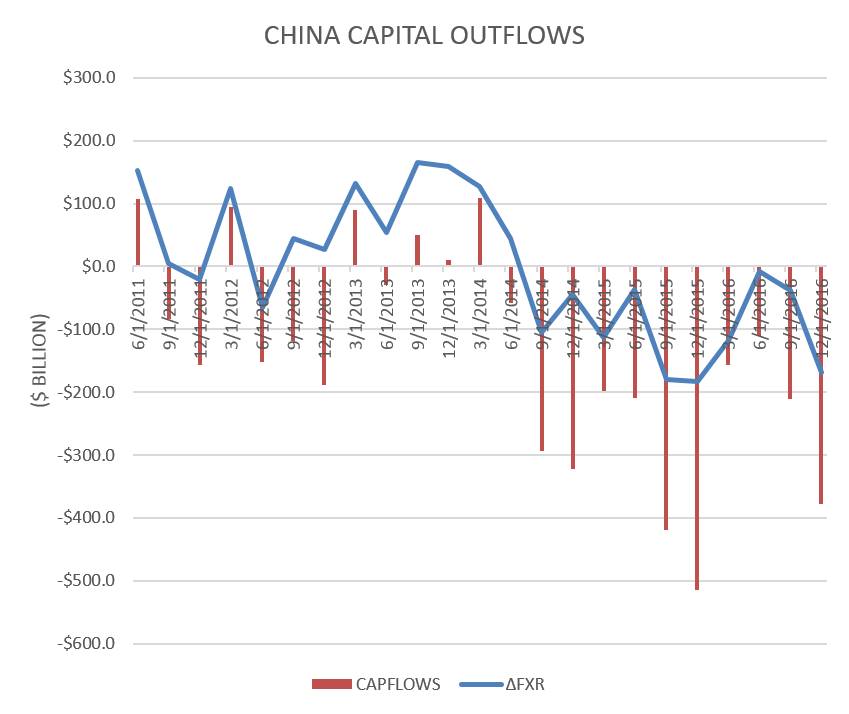

Despite the efforts at stabilizing the yuan’s depreciation, China continued to bleed foreign exchange reserves, which fell from a peak of about $4 trillion in to under $3 trillion at the end of 2016. If we factor in the significant current account surpluses accumulated over this period, the total capital outflows from July 2015 to-date totaled $1.8 trillion dollars ($2.9 trillion since mid-2014). Also, the combined capital and current account deficit excluding foreign direct investment (FDI) reached $176 billion, with FDI reaching only $32 billion over the period.

Alarm over the rapid loss of foreign exchange reserves and the continued depreciation of the yuan led the Chinese foreign exchange regulator (the State Administration for Foreign Exchange, SAFE) to reintroduce increasingly strict capital control measures to stem the capital outflows at both the retail and corporate levels in the past few months. While the individual annual quota of $50,000 levels was maintained, SAFE limited its use—e.g., the foreign exchange could not be used for foreign property purchases. Banks’ foreign currency lending was subject to a balance between inflows and outflows, and outward direct investment (ODI) was scrutinized to weed out fake ODI. Foreign corporations also reported problems in repatriating profits. Finally, the PBoC raised short-term interest rates in early February. However, these measures, which represent a retreat from market liberalization, will not be enough in themselves to prevent a further weakening of the yuan.

While these measures stabilized the situation somewhat in early 2017, they also illustrate the complexities faced by China in in its efforts to internationalize the yuan. At the same time, irreversible market forces are at play, and controlling (or manipulating) the currency is increasingly a fool’s errand. The yuan’s level will increasingly be determined by macroeconomic and market fundamentals, not by the PBoC, and attacking China for currency manipulation is really flogging a dead horse.